Just a quick update on the performance of the Lazy Portfolios through Halloween. What a move they have had since August. Is it a repeat of the move that we saw from Feb – Apr? I’ll update you in a couple of months and we will find out. In the meantime, I don’t really care because the Permanent Portfolio allows me to not worry about the economy, the markets, or the FED.

ID#

Portfolio Name

YTD Return

P2

Paul Boyer Permanent Portfolio (ETF)

13.9%

P3

Permanent Portfolio Fund (PRPFX)

13.8%

P14

David Swensen’s Yale Endowment

12.8%

P19

Scott Burns’ Four Square Portfolio

12.8%

P24

IFA Index Portfolio 100 Bright Red

12.7%

P1

Harry Browne Permanent Portfolio (ETF)

12.7%

P9

Dilbert World’s Simplest

11.4%

P20

Scott Burns’ Five Fold Portfolio

11.3%

P13

David Swensen’s Lazy Portfolio

11.2%

P10

Ted Aronson’s Lazy Portfolio

11.0%

P15

MMM Do It Yourself Funds

10.8%

P11

Bill Schultheis’ Coffeehouse Portfolio Vanguard

10.7%

P22

Larry Swedroe Simple

9.9%

P6

Rick Ferri Core Four

9.7%

P21

Scott Burns’ Six Ways from Sunday Portfolio

9.5%

P12

FundAdvice Ultimate Buy & Hold

9.4%

P17

Scott Burns’ Couch Potato Portfolio

9.3%

P7

William Bernstein’s No Brainer Cowards Portfolio

8.7%

P23

Larry Swedroe Min Fat Tails

8.6%

P18

Scott Burns’ Margarita Portfolio

8.6%

P5

Taylor Larimore 4 Fund

8.5%

P25

IFA Index Portfolio 50

8.4%

P4

Taylor Larimore 3 Fund

8.3%

P8

William Bernstein’s Basic No-Brainer Portfolio

7.7%

P16

Vanguard Windsor

6.2%

Mon, November 1 2010 » Analysis, Blog » Comments Off on Lazy Portfolios Through October 2010

Craig at Crawlingroad.com/blog has just released episode one of a new podcast that talks about the Harry Browne Permanent Portfolio. I encourage you to subscribe to it in iTunes and listen to every episode he puts forward in the future. It is going to be great.

Use this link to subscribe in iTunes (copy and past it into iTunes using the Advanced -> Subscribe to Podcast… menu:

http://www.crawlingroad.com/podcasts/podcasts.xml

Tue, October 26 2010 » Announcements, Blog » Comments Off on Subscribe to the Crawling Road Money Show Podcast

Instead of using Standard Deviation as the measure of a portfolio’s risk, I have been looking at using Max Drawdown which I believed could be more user-friendly. Standard Deviation involves complicated statistical computations. Could you explain Standard Deviation to your grandmother? Max Drawdown would be easier to explain. It is the largest peak to trough drop in a portfolio, measured in percentage. For example, if the largest drop of a portfolio during a studied time period was from $100,000 to $60,000, that would be a Max Drawdown of 40% for that time period.

Recently, I have been computing the Max Drawdown of the many Lazy Portfolios. I modified Simba’s spreadsheet to include monthly returns data instead of just yearly data because a portfolio could suffer drawdown within the year and recover before the end of the year, thus masking the fact that a larger drawdown occurred.

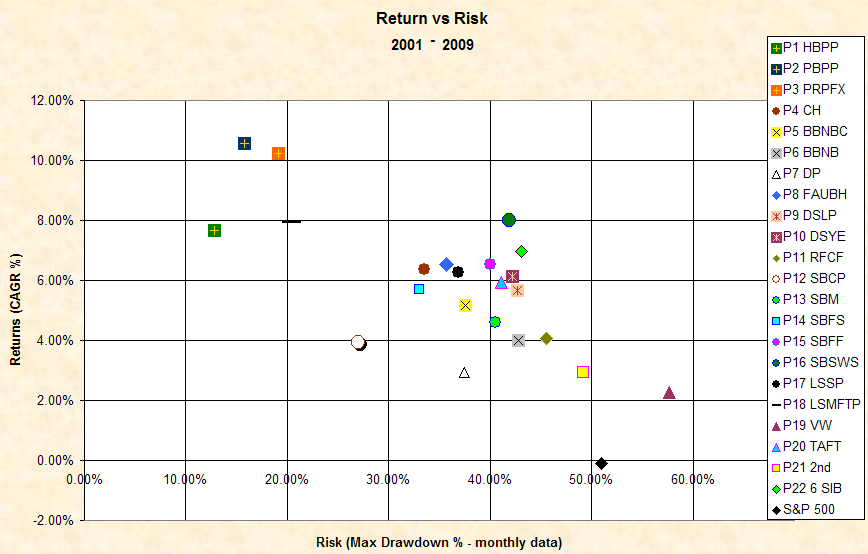

The following chart shows the Annualized Returns vs. Monthly Max Drawdown for several Lazy Portfolios from the beginning of 2001 through the end of 2009. (I am in the process of renumbering the Lazy Portfolios, so this post does not correlate with previous posts. See the Appendix for portfolio names.)

Figure 1: Annualized Return vs. Monthly Max Drawdown 2001 – 2009. Click it for a larger chart. See the full legend below.

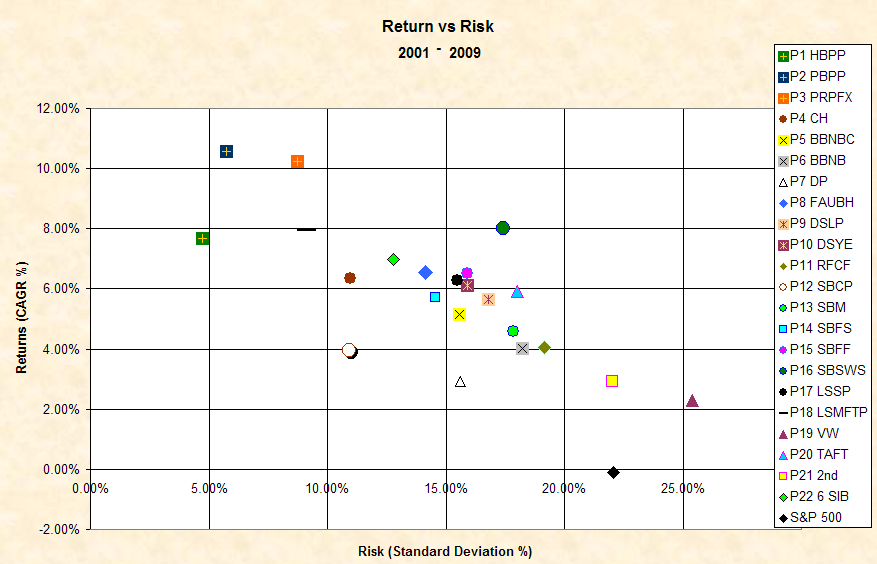

This next figure is the more traditional chart showing Annualized Returns vs Annualized Standard Deviation in percent.

Figure 2: Annualized Return vs Annualized Standard Deviation 2001 – 2009. Click it for a larger chart. See the full legend below.

The ideal location of a portfolio’s plot point would be at the top left of either chart.

I was really surprised that these two charts looked so similar. Most of the Lazy Portfolios are in the same relative location on both charts. There are some small variations for select plots, but overall the chart looks the same. The biggest part of my surprise is that the Max Drawdown chart used monthly data and the Standard Deviation chart used only end of year data. Specifically, the Max Drawdown chart used 83 sample points while the Standard Deviation chart used only 9. The similarity of the charts gives me confidence that using Standard Deviation as a measure of risk is appropriate for evaluating the relative performance vs. risk of the Lazy Portfolios.

However, in terms of human understandability, I like Max Drawdown better because one can immediately apply the number to their own situation. It is simply a matter of multiplying one’s portfolio value by the Max Drawdown percentage. For example, for a peak portfolio value of $100,000 invested in the PBPP, the Max Drawdown during the period was about $15,000. That number is understandable. It also is easy to compare the Max Drawdown of PBPP to the Max Drawdown of the Rick Ferri Core Four portfolio, for example, which dropped about $45,000.

The problem with Max Drawdown is that computing it requires many more sample points to get the actual value. I had previously computed Max Drawdown using only year-end values. When I did that, the Max Drawdown of the PBPP was only 0.5% compared to about 15% for using month-end values. It turns out that the PBPP dropped about 15% in 2008 but recovered most of it before the end of the year. Even so, Obviously we would need daily values to get the true maximum number. Even so, a chart of Max Drawdown using only year-end values showed the same relationship between the Lazy Portfolio plot points.

Max Drawdown is an easier risk number to comprehend than standard deviation. But it is more difficult to compute. And the relationship between the portfolios’ risk remains largely the same.

Appendix

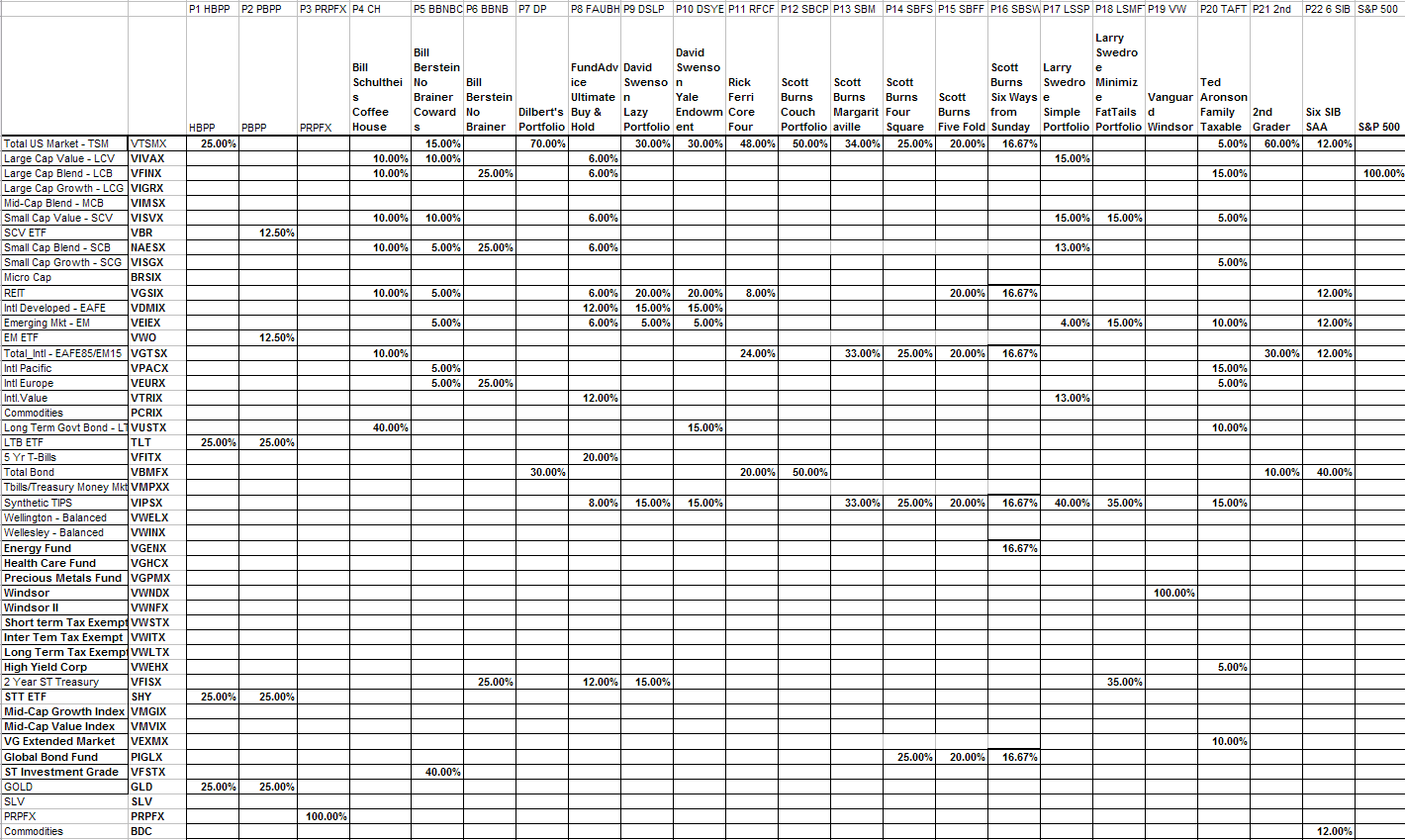

The following table lists the legend key for each plotted Lazy Portfolio along with its full name.

Legend Key

Portfolio Name

P1 HBPP

Harry Browne Permanent Portfolio

P2 PBPP

Paul Boyer Permanent Portfolio

P3 PRPFX

Permanent Portfolio Mutual Fund

P4 CH

Bill Schultheis Coffee House

P5 BBNBC

Bill Berstein No Brainer Cowards

P6 BBNB

Bill Berstein No Brainer

P7 DP

Dilbert’s Portfolio

P8 FAUBH

FundAdvice Ultimate Buy & Hold

P9 DSLP

David Swenson Lazy Portfolio

P10 DSYE

DavidSwenson Yale Endowment

P11 RFCF

Rick Ferri Core Four

P12 SBCP

Scott Burns Couch Portfolio

P13 SBM

Scott Burns Margaritaville

P14 SBFS

Scott Burns Four Square

P15 SBFF

Scott Burns Five Fold

P16 SBSWS

Scott Burns Six Ways from Sunday

P17 LSSP

Larry Swedroe Simple Portfolio

P18 LSMFTP

Larry Swedroe Minimize FatTails Portfolio

P19 VW

Vanguard Windsor

P20 TAFT

Ted Aronson Family Taxable

P21 2nd

2nd Grader

P22 6 SIB

Six Core Asset Index Funds Strategic Asset Allocation Moderate

S&P 500

Standard & Poors 500 Index

Here is the spreadsheet of each portfolio’s holdings. Click to make it readable. Someday I will update this web site to show the contents of each of these Lazy Portfolios in HTML format.

Data is from Yahoo! Finance historical adjusted returns. Actual data used where possible. Data prior to inception for VBR used VISVX, VWO used VEIEX, TLT used VUSTX, GLD used gold, SHY used VFISX. The data and the resulting analysis may contain errors. Invest at your own risk.

Fri, October 22 2010 » Analysis, Blog » Comments Off on Max Drawdown in Lazy Portfolios 2001 – 2009

At the Bogleheads 9 Reunion in Philly this past week, I had the opportunity to show Dr. Bill Bernstein the first part of the video we put together that featured Dr. Bill Bernstein’s quote. He laughed and laughed. And he signed my copy of his book.

And here is the video:

Sat, October 16 2010 » Blog, Video » Comments Off on Bernstein Views Bernstein

I have the rare privilege of attending the Bogleheads 9 reunion in Philly this year. I wanted to attend the one much closer to my home a couple of years ago, but was way too late in registering. They only let 120 or so folks attend these things. So I registered early enough this year and I thought it might be helpful if I could share some of the things I’ve heard today and will hear tomorrow. At least I’ll be able to remember them better this way.

Today (Thursday, 14 October) was basically Jack Bogle Day. Sure, we heard some about how the Bogleheads got started and we even took the time to go around the meeting room and have every person in attendance tell something about themselves. In addition to Jack Bogle, also in attendance are some authors of investing books you may know: Bill Bernstein, Bill Schultheis, Rick Ferri, and the authors of the various Bogleheads books.

But immediately after the introductions, Jack showed up a little early. Don’t think me presumptuous for using his nickname, that is what he prefers. He spoke with some prepared remarks for about an hour or so and then took questions for another hour or so. We had lunch, then he and Bill Bernstein answered some more questions. He then gave each of us a copy of his new book “Don’t Count On It!” Subtitled Reflections on Investment Illusions, Capitalism, “Mutual” Funds, indexing, Entrepreneurship, idealism, and Heroes. Then we stood in line to have Jack sign his name and we spoke with all of the other authors present.

Here are some representative notes and quotes I took from Jack’s talk.

“Mutual fund companies are run for the benefit of the managers and not the benefit of investors.” Except, of course, one mutual fund company…

“Last year Fidelity managers made $2.6B and Vanguard managers made $0.” [Correction: he said Fidelity’s earnings were $2.6B]

He showed a chart of how Vanguard’s average expense ratio keeps dropping. But noted that now with the size of assets under management, one basis point equals $140M. So it would be easy to say, “Let’s spend $140M on something, they’ll never know.” So Jack recommends they think in terms of dollars and not in terms of basis points.

He said, “Keeping expenses low is a simple, moronically simple, yet it is an idea that nobody thought of.”

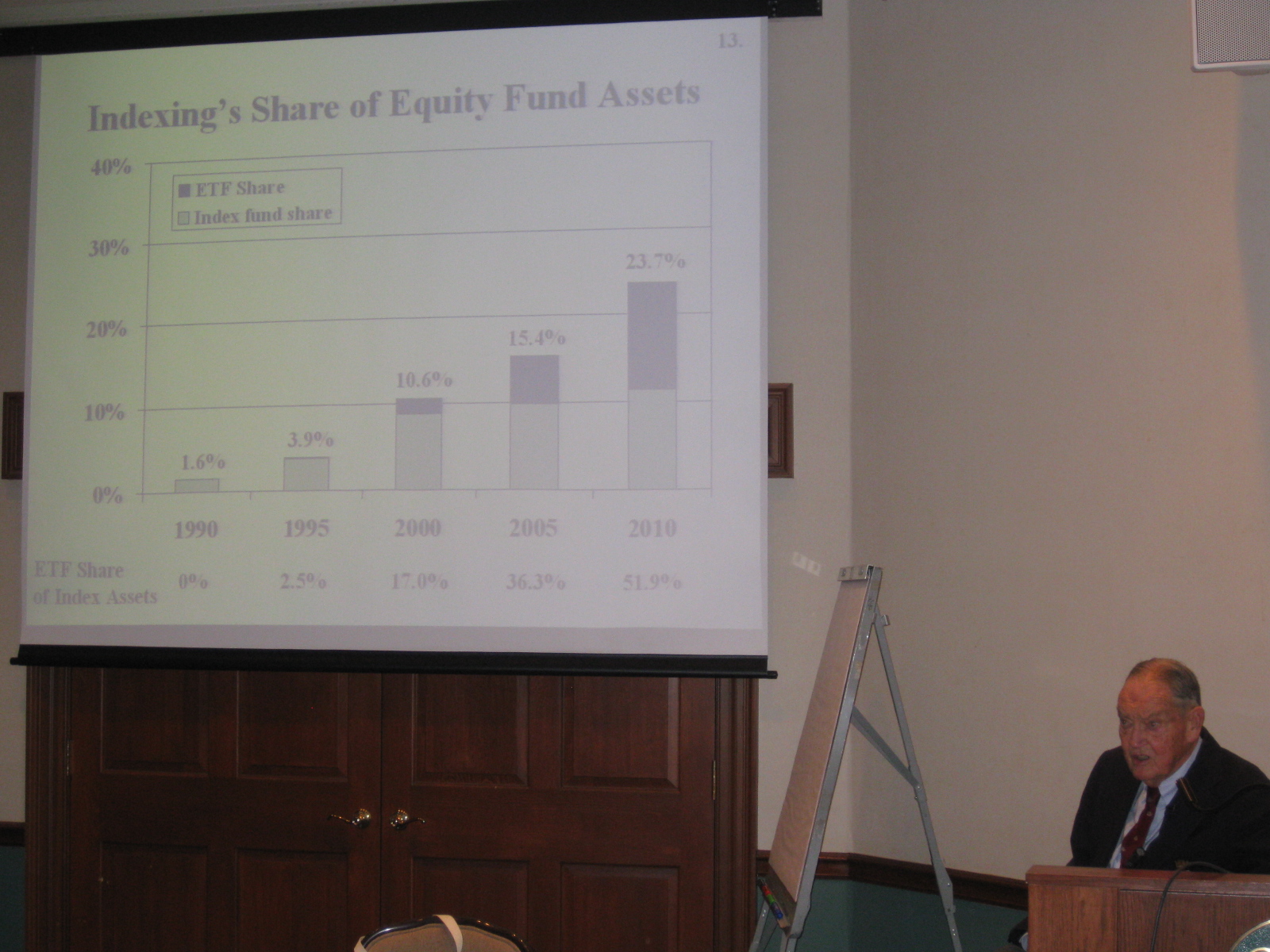

He said that in 2010, ETF’s share of the index market matches the index fundshare. ETF share of index assets is 51.9%

On the topic of holding assets for the long term, he said, “One firm holds its assets for an average of 11 seconds. I don’t know how you feel about that, but that’s not long term investing.”

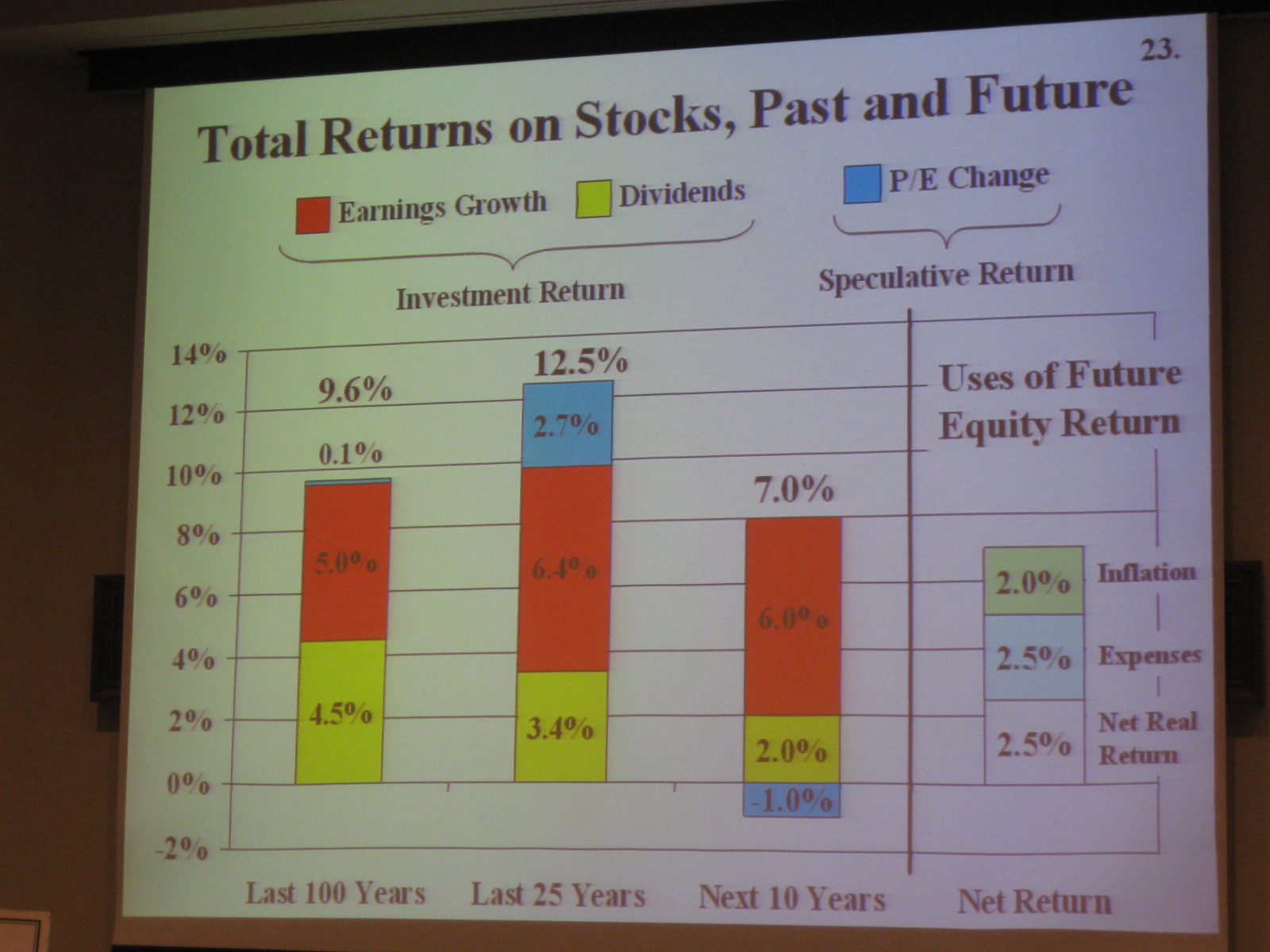

“There is no place to hidethese days. Never seen anything like it. Assuming we don’t have a big disaster, which is a big assumption to me,we will see 2.5% real returns on equities in future (after inflation and expenses).”

“Gold was a terrible investment over 100 years. Rank speculations. I am almost tempted to buy gold but I won’t. 1 or 2 or even 5% to play with is OK.”

“I am a little worried about the risks that are still out there. US Financials is a mess. Pensions are bankrupt. Don’t see how they will get 8%. Wall St. Values are in tatters. America has lost ability to govern itself. I find a lot of resonance when I speak about values. I find young people are seeking something nobler. I am hoping to make a tiny difference in values.To get a financial system that works for all of you and not Wall St.”

“Rebalance? Data says don’t bother. Maybe if you need a 50/50 portfolio and it gets to 60/30 then rebalance if you need to.”

“The power of money in Washington is disgusting.”

“I think about what is going on with Emerging Market funds. They are among the largest ETFs. The Data said 33% of all EM holdings were in ETFs. Makes me worried because ETF owners are traders. Suppose something happens to Brazil and traders decide to get out. Could be a big… Still, in the long run that should not matter. If EM is held up by Mutual fund demand, when they go it could cause trouble. Vanguard should be careful when getting into these funds.”

Finally, Bill Schultheis, the author of The Coffeehouse Investor, stood up and asked a question of Jack and Bill Bernstein. It was about the disaster of 401K plans for the average citizen. How they don’t understand how to invest their own money. And would Jack and Bill recommend a more managed approach. Bill answered first and said, “The less autonomity the better. Don’t let people run their own funds. I want a big maternalistic approach.” Jack basically agreed and listed a few points about 401(k) plans: “1. You’re going to borrow money from it 2. You will take it out. 3 you don’t have to contribute to it 4. The investor has no guidance . With the average 401k being $54,000, have a great retirement.” Jack prefers the idea of a privatized personal retirement plan like former President George W. Bush initially suggested.

I asked Jack about his thoughts on the future of the US Dollar and the Federal debt and how that would affect the investor. Would we see hyperinflation? He answered that currency speculation is not something to get into. That we would want the dollar to fall relative to China. That China owns a large amount of our bonds and they may fall in value if interest rates rise. He repeated that he should probably buy some gold for insurance (against the US Dollar) but that he is just “too busy” to do it.

It has been great being here at the Bogleheads 9 reunion. Everyone is nice to talk with and with such a small gathering, we have lots of time to talk to everyone.

Thu, October 14 2010 » Analysis, Blog » Comments Off on Some Observations From Bogleheads 9 and From Jack Bogle Himself

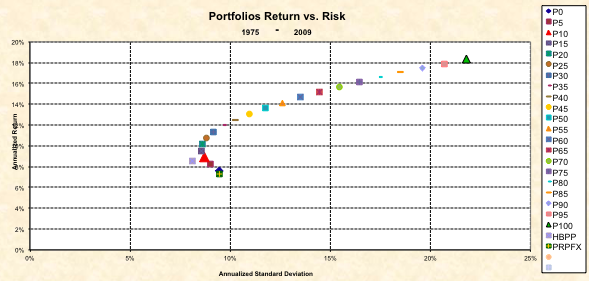

You gotta own some stocks, but how much? I took the Paul Boyer Permanent Portfolio and varied the percentage of stock ownership from 0% to 100% in 5% increments while keeping gold, long term bonds, and cash divided equally among the remaining amount. Then I plotted each portfolios return vs. risk for 1975 through 2009. Take a look at the resulting graph. It turns out that portfolios with less than about 25% stocks were generally the same level of risk or even (surprise) a higher level of risk than holding 25% stock. Each of the numbered portfolios P0 through P100 split their stock ownership between Small Cap Value (VISVX) and Emerging Market (VEIEX). I also plotted the pure Harry Browne Permanent Portfolio and a simulated PRPFX.

It looks like Harry Browne was really onto something with his recommendation of owning 25% in stocks.

Mon, October 11 2010 » Analysis, Blog » Comments Off on Proof You Gotta Own Some Stock

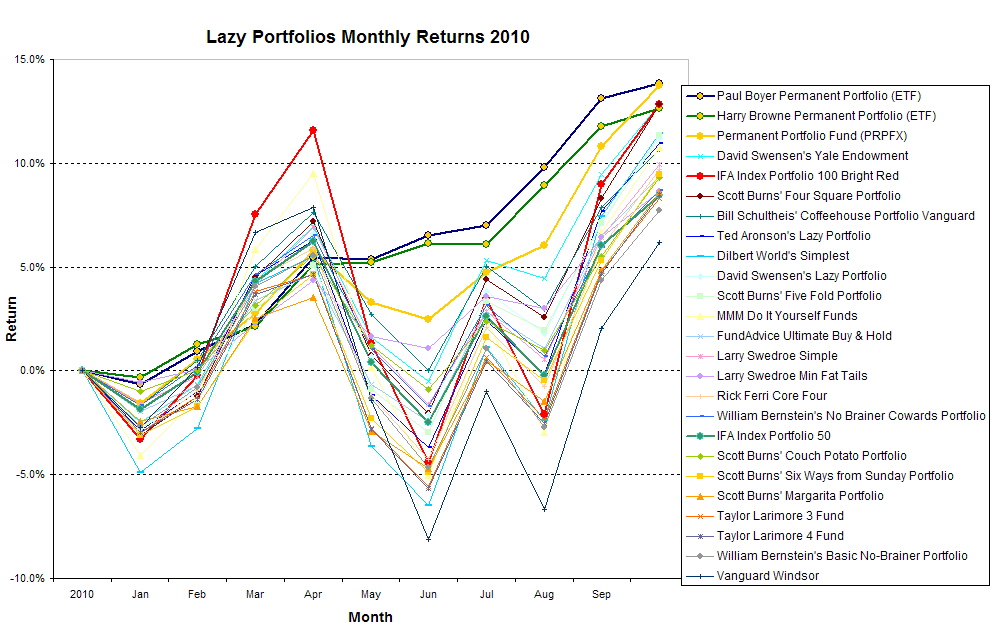

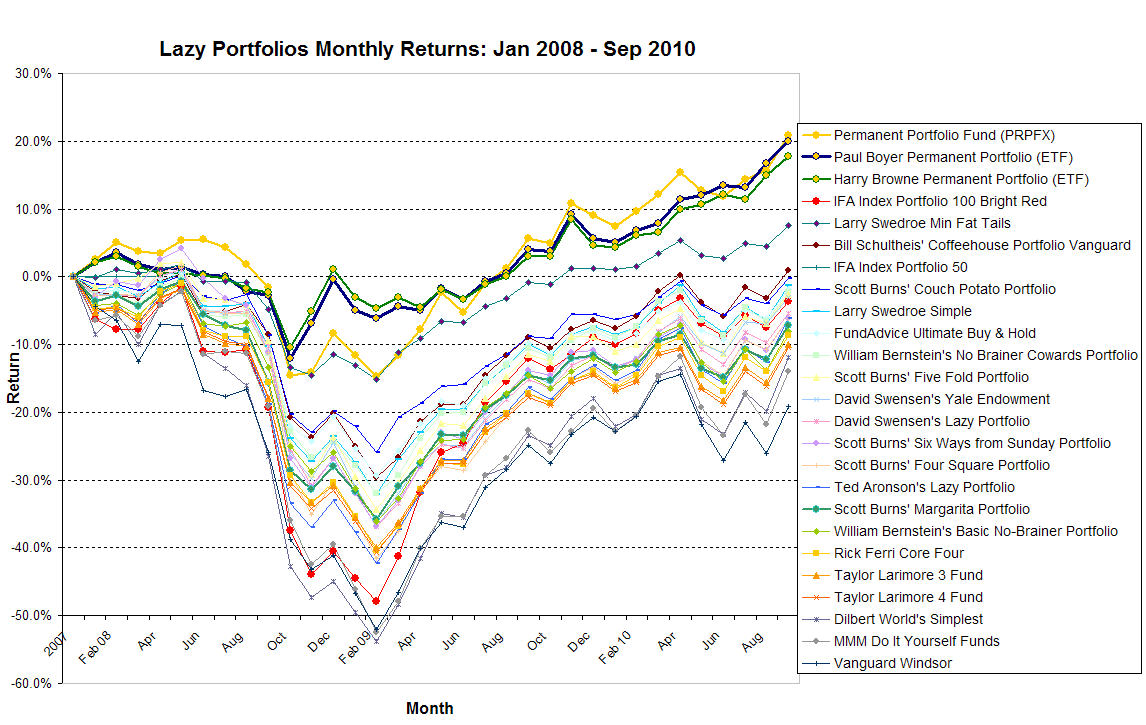

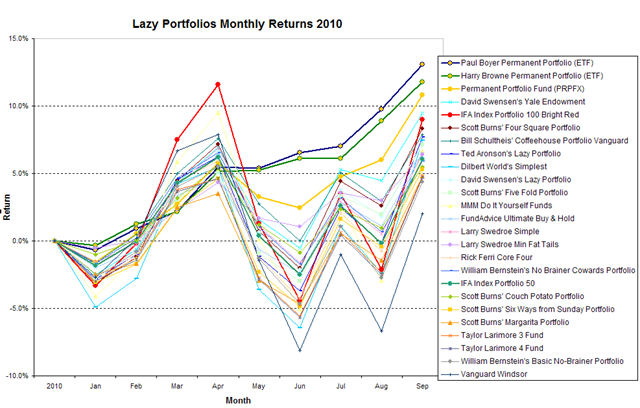

Here is a chart plotting the end-of-month returns for the lazy portfolios. Wow, what a roller coaster ride if your portfolio was 100% in stocks. On the other hand, wow, what a nice smooth ride if you were in one of the three permanent portfolios. The Paul Boyer Permanent Portfolio remains in the lead with an amazing 13.1% gain through the first three quarters of 2010. Look at that steady upward blue line! Thank you Harry Browne.

And here is the table of returns through September 2010:

ID#

Portfolio Name

YTD Return

P2

Paul Boyer Permanent Portfolio (ETF)

13.1%

P1

Harry Browne Permanent Portfolio (ETF)

11.8%

P3

Permanent Portfolio Fund (PRPFX)

10.8%

P14

David Swensen’s Yale Endowment

9.5%

P24

IFA Index Portfolio 100 Bright Red

8.8%

P19

Scott Burns’ Four Square Portfolio

8.3%

P11

Bill Schultheis’ Coffeehouse Portfolio Vanguard

7.9%

P10

Ted Aronson’s Lazy Portfolio

7.7%

P9

Dilbert World’s Simplest

7.4%

P13

David Swensen’s Lazy Portfolio

7.2%

P20

Scott Burns’ Five Fold Portfolio

7.1%

P15

MMM Do It Yourself Funds

6.7%

P12

FundAdvice Ultimate Buy & Hold

6.5%

P22

Larry Swedroe Simple

6.4%

P23

Larry Swedroe Min Fat Tails

6.4%

P6

Rick Ferri Core Four

6.0%

P7

William Bernstein’s No Brainer Cowards Portfolio

5.9%

P25

IFA Index Portfolio 50

5.9%

P17

Scott Burns’ Couch Potato Portfolio

5.5%

P21

Scott Burns’ Six Ways from Sunday Portfolio

5.3%

P18

Scott Burns’ Margarita Portfolio

4.8%

P4

Taylor Larimore 3 Fund

4.8%

P5

Taylor Larimore 4 Fund

4.7%

P8

William Bernstein’s Basic No-Brainer Portfolio

4.4%

P16

Vanguard Windsor

2.0%

Data on IFA portfolios is courtesy of ifa.com. All other portfolio returns are calculated using Yahoo! Finance historical returns and may not include dividends paid in the most recent month.

Fri, October 1 2010 » Analysis, Blog » Comments Off on Lazy Portfolios Thru September 2010

How can you properly determine if your investment have met your expectations?

Watch “Proper Benchmarking and Alpha” for a lesson on measuring risk against a complete set of important factors. These videos are based upon IFA’s Quote of the Week Issue #82.

Part 1:

Part 2:

Thu, September 30 2010 » Blog, Tips, Video » Comments Off on Video Lessons: Proper Benchmarking and Alpha

VERTIGO! Listen to Shrugging Out podcast. OLD: D vs. R. New: P vs L. Inflation or deflation? A cool tool. A cool Guru. I ENCOURAGE you to Download this show thru iTunes! But, if you just cannot deal with that then go ahead and Play the new show right now

Things I consume: Shrugging Out podcast is one worth checking out. Pete really has a rational head. No-nonsense discussion of what is happening. Some real gems of shows in his podcast catalog.

Also, No Agenda, Glenn Beck, Lew Rockwell, Freetalk Live, Alex Jones, Freedom Watch, Stossel.

Democrats vs. Republicans is no longer the divide. Today it is Big Government vs. Libertarian ideas.

Permanent Portfolio review.

We can’t predict the future, so invest in all possibilities.