Book Review: Jim Cramer’s Stay Mad for Life

You can understand why this book was written, can’t you? It’s like a shampoo brand that demands you use it in conjunction with their conditioner. Yet the more you wash and condition, the greasier your hair feels. So you gotta wash again. Jim Cramer’s Stay Mad for Life: Get Rich, Stay Rich (Make Your Kids Even Richer) promotes the TV show. The TV show promotes the book. ‘Round and ’round. Slap down 261 pages of stream-of-consciousness stock talk, put Jim’s bald head on the cover with his mouth open and hands in the air, and include the word "Mad" in the title. Reach an Amazon rank of 15 or so. Jim works himself into a lather. We rinse. He repeats next Christmas. But it’s a bad hair day.

Amazon.com: Jim Cramer’s Stay Mad for Life

Amazon.com: Jim Cramer’s Stay Mad for LifeWe already have a Cramer book telling us to beat the market by picking stocks (Jim Cramer’s Real Money) and a book telling how to watch his TV show (Jim Cramer’s Mad Money). So what’s left for this Christmas season? Jim telling us that we need to save money. Jim telling us to make a budget. Jim telling us to invest in our 401(k). Jim telling us to buy bonds. Jim telling us to get a good mortgage. Jim telling us to buy stock for our children!

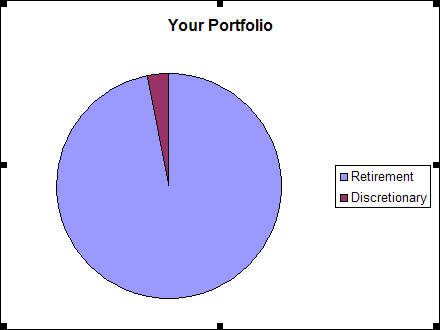

Jim states up front the distinction between discretionary vs. retirement money. And while there are no charts anywhere in the book, he should have put a pie chart in that looks something like this:

And then go on to say that on his TV show and in his previous books he was focusing on that tiny slice of Discretionary money or "Mad Money" that is exciting, thrilling, fun (and lucrative for those who sell their ideas about which stocks to gamble upon). In the first few chapters he tells us that we should save, budget, and invest in a 401K to take care of most of the pie. And then in later chapters he gets back into his shtick of picking out the winning stocks and actively managed mutual funds for the tiny slice.

In many places his advice is confusing, such as when he takes both sides of an argument. Are index funds good or bad? Page 104:

Then there’s the index funds crowd that still believes in owning stocks, but not picking them. Their attitude is just another example of sour grapes… You can still read columns by people who think something like this: Only a tiny minority of mutual funds consistently beat the indexes, and if the pros can’t do it, it’s no wonder I screwed up, so you’ll screw up too! These types know that stocks are winners, but don’t believe anyone can consistently tell good stocks from bad, so they give up and smugly buy an index fund. Then they act like those of us who pick stocks are dopes for even trying. They can call us dopes all the way to the bank.

Then on page 126:

With very few exceptions, I’m a strong advocate of owning index funds. I think John Bogle, the man who created the first modern index fund and opened up indexing to nonprofessionals, is both a genius and, from what I saw when I brought him on my old TV show Kudlow & Cramer, a really good guy. Even if Bogle were a jerk, he’d still be right about index funds. If you really cannot or will not spare the time and energy to research and own stocks, index funds are a great way for you to get exposure to pretty much everything you need….

In any case, index funds are terrific.

Whew, my shampooed and conditioned head is spinning!

After getting all the Suze Orman-like material out of the way in the first few chapters, he goes into his tried and true collection of sure-fire rules for better investing. Similar to Real Money‘s twenty-five rules, this time he presents twenty rules. Some are repeats familiar: "Never turn an investment into a trade." (like "Never turn a trade into an investment") Some appear to contradict previous rules: "If you buy a position to fill a need in a portfolio, don’t jettison it because it’s not working" replaces this rule from Real Money: "Your first loss is your best loss." If you are looking to invest by cracking open fortune cookies, here’s the book for you.

He continues with "Ten Things Pros Do Right but Amateurs Get Wrong." Number 9: "Pros know that cuffing it without doing homework can reduce you to–well, no offense–an amateur!" This is Jim’s catch-all safety net any time someone complains that the stock or mutual fund they bought upon his recommendation didn’t work out: You didn’t do your homework!

The final two chapters give us twenty specific stocks and a dozen or so specific mutual funds. They seem to focus on US stocks. What about the international or emerging markets Jim? He does mention that we should get into US stocks that have good international exposure so that "regardless of what’s happening in the domestic economy, regardless of all that chatter you hear endlessly about what the Federal Reserve might do or what the growth of the nation is or what the next quarters look like, these bull markets will hold up on their own." Yes but they are all still denominated in dollars. How about diversifying into stocks denominated in their local foreign currency?

Nonetheless, Jim’s specific recommendations are going to be fun indeed to watch over the long term and see whether they beat or lag a passive investing approach. My prediction is that they won’t beat the indexes and that all the time wasted doing stock picking homework and reading his books and watching his TV show could have been spent on more constructive pursuits. Like washing that man right out of our hair.

So, who wants to win a copy? I’ve got two more to give away. Make a comment here or write something on your blog referencing MadMoneyMachine.com and I’ll enter your name to win on show 90.

Paul – You forgot to put the time allocation pie chart to accompany the Your Portolio Chart. Jim Cramer implies we should spend 99% of our invetment time (e.g. Jim Cramer’s homework) on the Purple slice of the Portolio chart.

It’s ok to use your time like that – just remember your return on time may not achieve your life/time objectives.

Great review. I will probably still read the book (when it hits the library).

From the excerpts that you pointed out, it definitely looks like Cramer is flip-flopping all over the place. No different than when he says to sell a stock because it is way over valued and then when it is $10 higher 4 months from his initial statement all of a sudden it is a “buy”.

With the way this market has been lately, being in specific stocks and having to check them daily is a nerve-wrecking place to be.

It also seems to be an interesting pattern. The choice of words in his book titles

Addict, real, mad, stay

Hmmmm…. maybe not the best recipe ‘for life.’