Permanent Portfolio to Perfect Portfolio?

Harry Browne’s Permanent Portfolio is so simple. Split your investments into equal parts stocks, bonds, cash, and gold. Is it too simple? Can it be improved yet remain simple? I used Simba’s spreadsheet (from Bogleheads.org) to back-test some alternatives from 1972 through 2009.

First, the original portfolio:

Stocks: VTSMX (Total US Stock Market)

Bonds: VUSTX (Long-term Bond)

Cash: VMPXX (Money Market)

Gold (Kitco 1972-2004, GLD 2004-2009)

yielded the following return vs. risk:

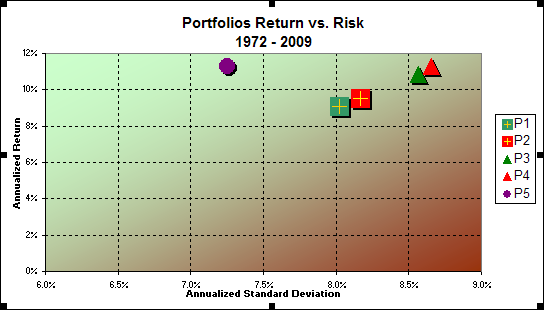

P1 (HBPP):

Compound Annual Growth Rate (CAGR): 9.1%

Standard Deviation (Risk): 8.02%

Sharpe Ratio: 0.46

Next, substitute 2-Year Short Term Treasuries (VFISX) instead of Money Market:

P2 (P1 with 2-yr T-Bills):

CAGR: 9.5%

Standard Deviation (Risk): 8.17%

Sharpe Ratio: 0.50

Alternatively, how about for the “Prosperity” component, i.e., Stocks, we substitute half US Small-Cap Value and half Emerging Markets for the US Total Stock Market:

P3 (P1 with 12.5% VISVX and 12.5% VEIEX):

CAGR: 10.8%

Standard Deviation (Risk): 8.57%

Sharpe Ratio: 0.64

And finally, combine P2 and P3 to have 2-yr T-Bills, US Small Cap Value, and Emerging Market:

P4 (P2 with 12.5% VISVX and 12.5% VEIEX):

CAGR: 11.3%

Standard Deviation (Risk): 8.65%

Sharpe Ratio: 0.68

And just for comparison I ran “Solver” on Simba’s spreadsheet to find the least risky portfolio that yielded 11.3% of that time span. It came up with the following mix:

VISVX (US Small Cap Value): 13.43%

VEIEX (Emerging Market): 14.30%

PCRIX (Commodities): 5.19%

VFITX (5-Yr T-Bills): 49.31%

VFISX (2-Yr T-Bills): 7.88%

Gold: 9.88%

Which resulted in:

P5 (Solver optimized portfolio):

CAGR: 11.3%

Standard Deviation (Risk): 7.25%

Sharpe Ratio: 0.80

And here is a chart with them all plotted, CAGR vs. Standard Deviaion (Risk):

I’ve played with lots of combinations of back-tested portfolios through many different time periods and one thing is common: substituting VISVX and VEIEX for VTSMX resulted in higher returns and a higher Sharpe Ratio. And short term T-Bills for cash also added nicely.

Note that I only show the Solver optimized portfolio (P5) for reference. I believe it strays too far from the Permanent Portfolio strategy to be safe going forward.

I talked about P4 on MMM-175: The Perfect Portfolio. While I am not yet invested in it, it is the one I am targeting. I do not expect a CAGR of 11.3% for the next 37 years, but if I can get 6% I will be very happy.

Join us on Facebook

Join us on Facebook Follow us on Twitter

Follow us on Twitter