Investments for Inflationary Times (to Come?)

The Austrian economists anticipated the present crisis. Should we listen to them when it comes to their predictions about what comes next? In one voice they are saying we will experience inflation unlike we’ve seen in the USA in over 100 years. Inflation is defined as the increase in the supply of money and credit. We are certainly experiencing an increase in the supply of money at present. But the draw-down of credit is counter-acting the monetary inflation and we are hovering in inflationary stasis at present.

Fed Chairman Ben Bernanke said the same thing on February 18th:

Some observers have expressed the concern that, by expanding its balance sheet, the Federal Reserve will ultimately stoke inflation. The Fed’s lending activities have indeed resulted in a large increase in the reserves held by banks and thus in the narrowest definition of the money supply, the monetary base. However, banks are choosing to leave the great bulk of their excess reserves idle, in most cases on deposit with the Fed. Consequently, the rates of growth of broader monetary aggregates, such as M1 and M2, have been much lower than that of the monetary base. At this point, with global economic activity weak and commodity prices at low levels, we see little risk of unacceptably high inflation in the near term; indeed, we expect inflation to be quite low for some time.

He acknowledged that they are inflating. But he threw a red herring into the mix by talking about weak economic activity and low commodity prices (Heh, except gold, right Ben?) trying to infer that they are somehow the cause of inflation. No, they are the result of inflation. Next, he went into how they will correct their inflation:

However, at some point, when credit markets and the economy have begun to recover, the Federal Reserve will have to moderate growth in the money supply and begin to raise the federal funds rate. To reduce policy accommodation, the Fed will have to unwind some of its credit-easing programs and allow its balance sheet to shrink. … However, the principal factor determining the timing and pace of that process will be the Federal Reserve’s assessment of the condition of credit markets and the prospects for the economy.

Bernanke recognized that the plane is in a nosedive and at the last minute he plans to push on the stick and go airborne again. I hope it is not a cloudy day when he has to judge how far the plane is from the ground. He wrapped up his thoughts on inflation and how to avoid it:

As we consider new programs or the expansion of old ones, the Federal Reserve will carefully weigh the implications for the exit strategy. And we will take all necessary actions to ensure that the unwinding of our programs is accomplished smoothly and in a timely way, consistent with meeting our obligation to foster maximum employment and price stability.

What do *you* think the chances are that the Fed will get all of the necessary actions right? Have they gotten the necessary actions right up to this point? Let us examine a scenario where they are not able to get it right and we do indeed experience undesirable inflation, which I will define to be anything above 5% annually.

How might the various asset classes be affected in times of inflation? To answer this question, I utilized Simba ‘s spreadsheet for back-testing portfolios (which I imported into Google Spreadsheets) to do a correlation between CPI (Consumer Price Index, the government’s official inflation number) and various stock fund, bond fund, and gold returns. The data in the spreadsheet uses annual returns of Vanguard index funds along with the yearly closing price of gold from the years 1971 – 2008. The spreadsheet already calculated the cross-correlation between each of the mutual funds and it lists the annual CPI index. So it was very easy to drop the CPI into one of the mutual fund slots and instantly see the correlation between every asset class and inflation. Here are the results, sorted by correlation:

| Asset Class | Ticker | Correlation | |

| T-BILL (money mkt) | VMPXX | 0.63 | |

| GOLD | GOLD | 0.52 | |

| Long Term Govt Bnd | VUSTX | -0.40 | |

| Short Term Trsry | VFISX | 0.28 | |

| Commodities | PCRIX | 0.25 | |

| 5 Yr T | VFITX | -0.24 | |

| Wellesley Fund | VWINX | -0.21 | |

| Wellington Fund | VWELX | -0.16 | |

| Small Cap Grwth | VISGX | 0.13 | |

| Total Bond | VBMFX | -0.12 | |

| Small Cap | NAESX | 0.11 | |

| EAFE Dev | VDMIX | -0.10 | |

| Europe | VEURX | -0.10 | |

| Intl Value | VTRIX | -0.10 | |

| EAFE85/EM15 | EAFE/EM | -0.09 | |

| 500 Idx | VFINX | -0.09 | |

| Large Cap Grwth | VIGRX | -0.07 | |

| Total Market US | VTSMX | -0.06 | |

| Simulated TIPS | S-TIPS | 0.06 | |

| Pacific | VPACX | -0.06 | |

| Emerg Mkts | VEIEX | -0.06 | |

| Large Cap Value | VIVAX | -0.04 | |

| Small Cap Value | VISVX | 0.04 | |

| REIT | VGSIX | -0.01 | |

| Windsor Fund | VWNDX | -0.01 | |

| Mid Cap | VIMSX | -0.01 | |

| Micro Cap | BRSIX | 0.00 |

The table shows those asset classes that were most closely correlated with the CPI at the top. Note in the third column that a value of 1 would mean the asset is perfectly correlated, -1 would mean perfectly correlated inversely (it went down exactly as CPI went up), and 0 means there was no correlation: it was random.

So we see that those assets that were most highly correlated with CPI were T-bills, gold, long-term government bonds (inversely), short-term Treasuries, and commodities. Everything else was below 0.25 correlation. Interestingly, micro cap stocks were totally uncorrelated with inflation.

So how did a portfolio of those assets perform during the years 1973-1981 in which CPI was 8.7, 12.3, 6.9, 4.9, 6.7, 9, 13.3, 12.5, and 8.9%?

I constructed a portfolio along the lines of the Harry Browne Permanent Portfolio (HBPP invests 25% each into total US stock market, long-term bonds, money market, and gold) but I added some small cap value, micro cap, and eliminated the long-term bond fund. I then back-tested that portfolio during those inflation years. Here is the portfolio what I came up with:

The Inflation Portfolio:

VISVX (Small Cap Value) 15%

BRSIX (Micro Cap) 15%

PCRIX (Commodities) 10%

VMPXX (Money Market) 45%

Gold 15%

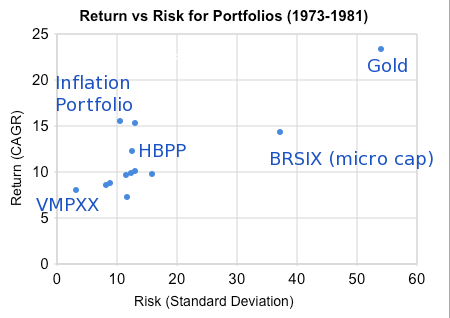

The "Inflation Portfolio" had a CAGR (Compound Annual Growth Rate) of 15.5% and a risk (as measured by standard deviation) of 10.5%. Plotting that on a chart, here’s what it looks like compared with some other portfolios and the assets themselves:

The chart shows plots for various portfolios during those inflation years. The plot point directly above HBPP simply substituted BRSIX for VTSMX in the HBPP. The major components of the Inflation Portfolio are also plotted separately showing how volatile gold and BRSIX were themselves. When tempered together with VMPXX, the risk came down considerably while retaining significant returns. You can see all of the rest of the details in the Google spreadsheet that I created for this scenario and you can test out other hypotheses yourself.

The Inflation Portfolio worked from 1973 through 1981. If we see inflation return, would it work again? Some folks are discussing these findings at the Bogleheads forum if you want to chime in.

Please note this is not a recommendation to invest your net worth in the Inflation Portfolio!