Lazy Portfolio Smackdown Update Jan 2008

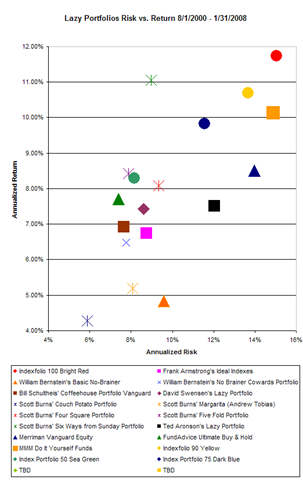

At the Lazy Portfolio Smackdown page, I have put in a table showing the returns of all entries into the game thru the end of January. No surprise that most of the portfolios are down. The exceptions being the clever China Bear portfolio and a commodities-heavy portfolio. What I intend to do is to show the standard deviations of these portfolios over the long term. That is hard to do for ETF portfolios, obviously. Here are the long term (well, since August 1st 2000 at least) risk vs. reward results for the professional lazy portfolios that invested in mutual funds.

Some of the IFA Index Portfolios are shown in circles. Notice how as the portfolios take on greater risk, they also achieve greater return. Notice how the IFA Index Portfolios generally have greater return for the same amount of risk than the other portfolios. There is a single outlier in the Scott Burn Six Ways from Sunday Portfolio. So let’s take a detailed look at it.

| Return | StDev | |||

| Vanguard Total Stock Mkt Idx | VTSMX | 16.7% | 1.03% | 14.07% |

| Vanguard Inflation-Protected Secs | VIPSX | 16.7% | 6.99% | 5.81% |

| Vanguard Total Intl Stock Index | VGTSX | 16.7% | 6.91% | 14.92% |

| Vanguard REIT Index | VGSIX | 16.7% | 14.58% | 15.08% |

| American Century International Bd Inv | BEGBX | 16.7% | 9.71% | 8.70% |

| Vanguard Energy | VGENX | 16.7% | 20.34% | 19.09% |

| TOTAL | 100.0% | 11.06% | 8.97% |

This portfolio returned 11% annually with 9% risk. So how did Scott Burns do it? Looks like he got a good return on bonds which have lower volatility than stocks while also getting great returns on REITS and in the specific sector of energy. How did his portfolio do recently? Also, not too bad. As you see on the Lazy Portfolio Smackdown page, the portfolio dropped only -2.91% in January. Again, those bond funds helped cushion the blow.

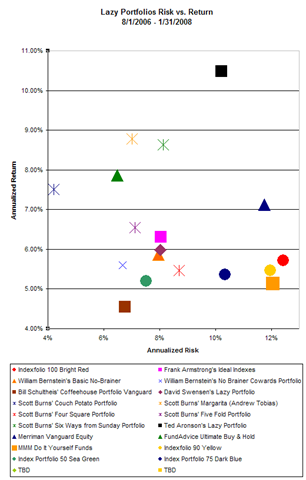

The following comparison takes a look at the portfolios since August 2006. This places more heavy emphasis on the poor performance of REITS and small cap US stocks in 2007. Not fair to compare them on such a short time span, but there it is.

We can see the out-performance of Ted Aronson’s heavily-weighted emerging market portfolio. It gained 10.48% with 10.21% risk in the 1.5 recent years. He has 20% in VEIEX the Vanguard Emerging Markets fund. It gained 28.63% over the period.

You can see the components of all portfolios on the Lazy Portfolio Smackdown page.

Join us on Facebook

Join us on Facebook Follow us on Twitter

Follow us on Twitter

Low Return = 3% plus (Risk/2)

High Return = 4% plus (Risk/2)

Anything within the 1% band is “efficiently” on the frontier. All others are either outstanding or requires improvement.

PS – The latest 5 yr Treasury auction yields 2.9% (e.g. the risk free rate)